What California Employees Should Know About Unpaid Commission Disputes

By Matthew J Ruggles

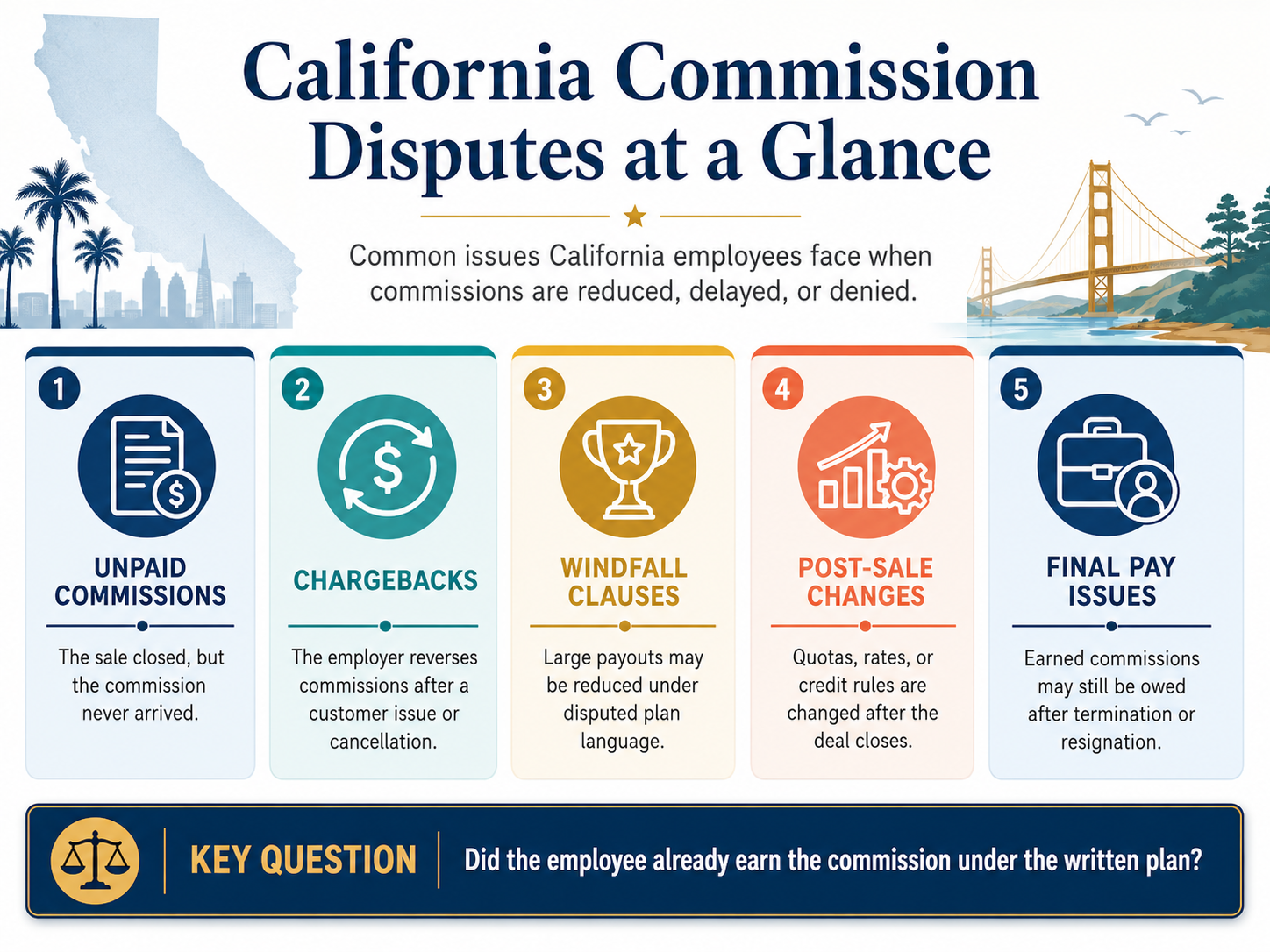

Why Commission Disputes Matter in California

A California commission dispute usually begins with a simple sentence: “This cannot be right.”

The employee closed the deal. The customer signed. Revenue hit the books. Maybe implementation started, maybe the invoice went out, maybe leadership celebrated the sale on a company call. Then, when payday arrives, the employer suddenly discovers a reason the commission is smaller, delayed, capped, clawed back, reclassified, split, or just missing. The explanation often arrives with impressive confidence and very little math, which is a classic corporate combination.

For California employees, commissions are not casual workplace favors. A commission is compensation for labor. California Labor Code section 200 defines wages broadly to include amounts owed for labor performed by employees, including compensation measured by time, task, piece, commission, or other method. Labor Code section 204.1 describes commission wages as compensation for services rendered in the sale of the employer’s property or services and based proportionately on the amount or value of the sale. Labor Code section 2751 requires written commission contracts for employees rendering services in California when compensation involves commissions, and the writing must explain how the commissions are computed and paid.

That framework matters because employers often try to make commissions feel discretionary after the employee has done the work. They may call the payment an incentive, an adjustment, a draw reconciliation, a windfall, a nonstandard deal, a discretionary payout, a management review item, a sales credit issue, a revenue recognition issue, or an administrative hold. Sometimes those terms matter. Sometimes they are legal fog machines. The job of a commission dispute is to separate enforceable plan language from post-sale improvisation.

This guide is written for California employees, especially high-earning commissioned employees, who are dealing with unpaid commissions, chargebacks, clawbacks, commission caps, windfall provisions, quota changes, split commissions, post-termination payout disputes, or employer retaliation after raising a commission issue. That includes enterprise software account executives, medical device sales representatives, financial services professionals, sales managers, regional vice presidents, CROs, technology executives, life sciences sales employees, and other employees whose compensation depends on large deals and complicated compensation plans.

For a shorter overview of unpaid commission recovery, read my post: California Unpaid Commissions Lawyer Explains How to Get Paid.

Commission disputes are not just about math. They are about leverage. A $30,000 commission dispute is serious. A $300,000 dispute can change a family’s finances. A seven-figure commission dispute can become the central employment-law issue in the employee’s career. The larger the number, the more likely the employer will suddenly become very creative. Creativity is admirable in jazz. It is less charming in payroll.

The most important question is usually not whether the employer thinks the commission is too large. The important question is whether the employee satisfied the objective conditions in the written commission plan. If the commission was earned, California wage protections may attach. If the payment was only an advance or remained subject to clear, lawful conditions, the analysis changes. The distinction can determine whether the employee has a strong wage claim, a contract claim, a retaliation claim, a waiting-time penalty claim, or a much harder argument.

Quick Answer: What Employees Should Know First

If you are in a California commission dispute, start with these core principles.

First, commissions are generally wages once earned. The California wage statutes are written broadly, and courts often focus on when the employee satisfied the conditions for earning the compensation. The employer’s label is relevant, but it is not always controlling. Calling something an “incentive” or an “adjustment” does not magically remove wage protections if the payment is actually a commission earned under the plan.

Second, the written commission plan usually controls. Labor Code section 2751 requires the plan to be in writing, to explain how commissions are computed and paid, and to be provided to the employee with a signed receipt. The plan should answer the most important questions: what sales count, what rate applies, when the commission is earned, when it is payable, what happens if the customer cancels, whether payments are advances, whether chargebacks are permitted, whether caps apply, whether management has discretion, and what happens after termination.

Third, ambiguity matters. California contract law generally interprets contracts to give effect to the parties’ mutual intent. Civil Code sections 1636, 1638, 1641, and 1644 require courts to examine the language, the whole contract, and the ordinary meaning of words. Civil Code section 1654 states that unresolved uncertainty is interpreted most strongly against the party that caused the uncertainty. In many commission disputes, the employer wrote the plan. That does not automatically mean the employee wins, but it can matter when the plan is vague, contradictory, or conveniently silent.

Fourth, chargebacks and clawbacks are not automatically illegal, but they are dangerous territory for employers. California cases such as Steinhebel v. Los Angeles Times Communications, LLC and Koehl v. Verio, Inc. recognize that an employer may structure commission payments as advances subject to later conditions when the plan clearly says so and the employee has not yet earned the commission. But once a commission is earned and paid as wages, Labor Code section 221 prohibits the employer from collecting or receiving back any part of wages previously paid, and cases such as Sciborski v. Pacific Bell Directory show why improper deductions can create serious exposure.

Fifth, windfall provisions and caps require careful analysis. A windfall clause may say the employer can reduce or cap commissions when the commission is unusually large, exceeds a percentage of quota, or results from an unusual transaction. Those provisions can be enforceable when clearly written and applied before the commission is earned or paid. But a vague windfall clause can also become a vehicle for after-the-fact wage reduction. The details matter. In commission law, the details do not live in the footnotes; they live in the paycheck.

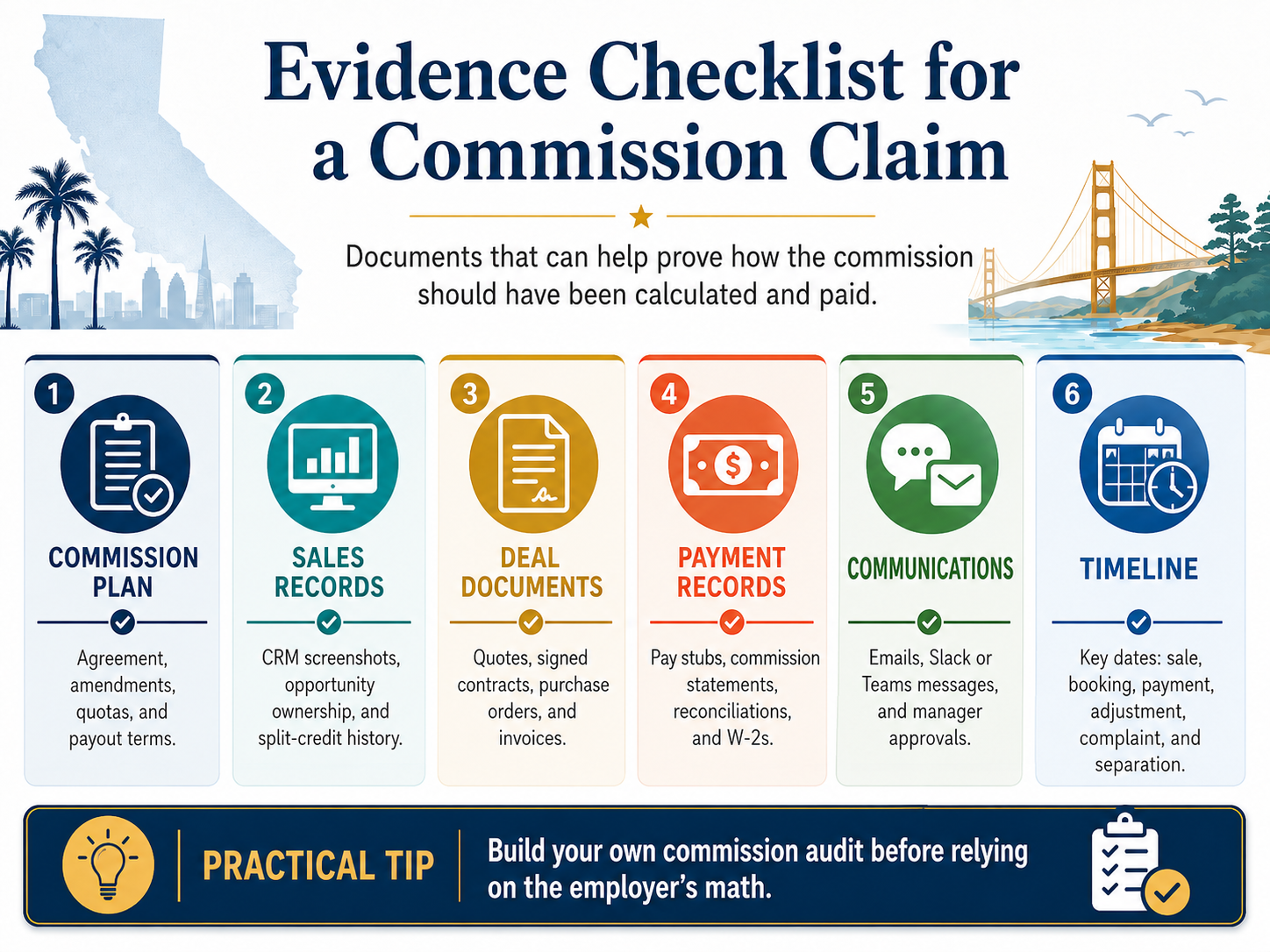

Sixth, employees should not rely only on the employer’s reconciliation. Build your own. Pull the commission plan, offer letter, quotas, plan amendments, CRM records, signed orders, invoices, payment records, pay statements, commission statements, emails about the deal, Slack or Teams messages, sales credit approvals, territory records, and any documents showing how similar deals were paid. The employer usually controls the accounting system. You need the receipts, preferably before the employer decides the receipts have entered the Witness Protection Program.

Seventh, retaliation is a separate issue. California Labor Code section 98.6 prohibits retaliation against employees who make written or oral complaints that they are owed unpaid wages. Labor Code section 1102.5 may also protect employees who disclose information about suspected legal violations to someone with authority to investigate or correct the violation. Employees should raise commission disputes professionally, in writing, and with facts. Do not rant. Do not threaten. Do not accuse everyone in accounting of joining a payroll cartel. State the issue, attach the documents, request the calculation, and preserve your evidence.

For a deeper discussion of windfall clauses, commission caps, and clawbacks, read my post: California Commission Clawback Lawyer for Employees: Windfall Provisions, Commission Caps, and Unpaid Sales Commissions.

What Counts as a Commission Under California Law

Not every incentive payment is a commission. That matters because commission rules do not automatically apply to every bonus, contest payment, SPIFF, discretionary award, retention payment, or profit-sharing plan. California Labor Code section 204.1 describes commission wages as compensation for services rendered in the sale of the employer’s property or services and based proportionately upon the amount or value of the sale. California courts have repeatedly looked for two central features: the employee is involved in selling property or services, and the compensation is tied proportionately to the amount or value of what is sold.

The leading cases illustrate why the definition matters. In Keyes Motors, Inc. v. Division of Labor Standards Enforcement, the court analyzed what constitutes a commission under California law and focused on whether the employee’s compensation was tied to sales. In Harris v. Investor’s Business Daily, Inc., the court examined whether a points-based compensation system qualified as a commission and emphasized that labels do not control the statutory definition. In Peabody v. Time Warner Cable, Inc., the California Supreme Court addressed commission wages in the context of pay-period compliance and rejected an employer’s attempt to attribute commission wages paid in one pay period to earlier pay periods.

A true commission typically involves a formula. For example, the employee earns 10 percent of gross revenue from qualified sales, 3 percent of net bookings, 7 percent of collected revenue, 15 percent of gross margin, or a fixed percentage of sales above quota. The formula may be simple or painfully complicated. A compensation plan can include tiers, accelerators, caps, gates, minimum margin requirements, customer payment conditions, customer retention conditions, product-specific rates, regional overrides, and revenue-recognition rules. Complexity does not make the plan unlawful. Complexity does, however, make it easier for the employer to hide the ball. Sometimes the ball is not hidden. Sometimes it has been buried under a 42-page spreadsheet named “Final_Final_Revised_Q4_v9.xlsx.”

Commissions are different from discretionary bonuses. A discretionary bonus may depend on the employer’s subjective judgment, overall company performance, or leadership approval. A commission is usually tied to sales activity and a formula promised in advance. That distinction is important because once an employee satisfies the conditions for earning a commission, California wage law may treat the commission as wages. The employer cannot avoid wage law by calling the commission a bonus if the plan actually promises a fixed percentage of sales or profits as compensation for work performed.

Labor Code section 2751 recognizes this distinction by excluding certain payments from its commission-agreement requirements. For purposes of that statute, “commission” does not include short-term productivity bonuses such as those paid to retail clerks, temporary variable incentive payments that increase but do not decrease payment under the written contract, or bonus and profit-sharing plans unless the employer offered to pay a fixed percentage of sales or profits as compensation for work to be performed.

Common commission structures include sales commissions, account executive commissions, channel commissions, override commissions, gross-margin commissions, net-revenue commissions, collected-revenue commissions, draw-against-commission plans, recoverable advance plans, accelerators, quarterly plan payouts, annual plan payouts, and management override commissions. Each structure can be lawful or unlawful depending on how it is written, disclosed, and applied.

The definition also matters for employees in hybrid compensation roles. Sales engineers, solutions consultants, account managers, customer success managers, regional directors, vice presidents, and executives may receive incentive pay tied partly to sales and partly to management performance. Some of those payments may be commissions; others may be bonuses. A single compensation plan may include both. Employees should not assume the entire plan has one legal character. A court or arbitrator may analyze each component separately.

The practical question is this: did the employer promise compensation based on a proportion of sales, revenue, bookings, gross margin, profits, or deal value? If yes, you may be dealing with a commission even if the employer used a more fashionable label. Corporate compensation departments enjoy inventing labels. The law cares more about function than branding.

For a practical overview of how these disputes usually get resolved, read my post: How Do I Resolve a Commission Dispute in California?

The Written Commission Plan: The Document That Usually Decides the Fight

In most California commission disputes, the written plan is the starting point, the roadmap, and the battlefield. It is not always the ending point, because statutes, case law, contract interpretation, public policy, retaliation law, and wage protections may also matter. But the plan usually tells you what the employer promised before the dispute began.

A strong commission plan should answer at least these questions:

- What sales, accounts, products, services, subscriptions, renewals, expansions, or renewals count for commission purposes?

- Who receives sales credit when more than one employee worked on the transaction?

- What commission rate applies to each category of sale?

- Are commissions based on bookings, invoices, collected revenue, gross revenue, net revenue, annual contract value, total contract value, gross margin, profit, or another metric?

- When is the commission earned?

- When is the commission payable?

- What conditions must occur before the commission is earned?

- What happens if the customer cancels, returns the product, defaults, fails to pay, delays implementation, or renegotiates?

- Are payments advances or earned commissions?

- Are advances recoverable, and if so, how?

- Are chargebacks permitted?

- Are commission caps, windfall clauses, or management-discretion adjustments permitted?

- What happens after resignation, termination, layoff, retirement, disability leave, or a territory change?

- How are disputes raised and resolved?

- What records are used to calculate commissions?

- Can the employer amend the plan, and if so, only prospectively or also retroactively?

If the answer to one of those questions is “ask finance,” that is not a plan. That is a scavenger hunt.

California Labor Code section 2751 requires a written commission contract when an employee renders services in California and the contemplated method of payment involves commissions. The contract must set forth the method by which the commissions are computed and paid. The employer must provide a signed copy and obtain a signed receipt. If the contract expires but the parties continue working under it, the terms are presumed to remain in full force and effect until the contract is superseded or employment is terminated by either party.

This statutory requirement matters because commission disputes often arise from ambiguity. Employers sometimes write broad provisions that reserve discretion over nearly every meaningful issue, then attempt to use that discretion after the employee closes a large sale. A plan might say commissions are subject to “management approval,” “company discretion,” “nonstandard deal review,” “special handling,” “reconciliation,” or “windfall adjustment.” Those phrases are not automatically invalid. But they should be interpreted in context and against the specific earning conditions. A plan that promises a fixed rate and then lets management reduce the commission for any reason may not be as flexible as the employer claims.

California contract law is important here. Civil Code section 1636 directs courts to interpret contracts to give effect to the mutual intention of the parties at the time of contracting. Civil Code section 1638 says clear and explicit language governs if it does not involve an absurdity. Civil Code section 1641 requires the whole contract to be read together. Civil Code section 1644 gives words their ordinary meaning unless a technical meaning applies. Civil Code section 1654 provides that unresolved uncertainty is interpreted most strongly against the party that caused the uncertainty. Since employers typically draft commission plans, ambiguity can become a powerful issue for the employee.

Employees should compare the plan against actual practice. Did the employer previously pay similar deals without a windfall cap? Did managers explain the earning conditions differently in writing? Did the CRM show the employee as the opportunity owner? Did finance issue preliminary commission statements confirming the amount? Did the employer celebrate the booking and then change the rules only after realizing the payout would be large? Those facts do not automatically override the written plan, but they can help interpret ambiguity, show inconsistent application, or undermine the employer’s explanation.

A commission plan should also be analyzed over time. High-earning sales employees often work under multiple documents: offer letter, annual plan, quota letter, compensation plan, incentive compensation terms, sales crediting policy, global commission policy, payroll policy, revenue recognition policy, employment agreement, arbitration agreement, and severance agreement. The employer may cite the one document most favorable to it. The employee should gather all of them.

The key is to create a timeline. What plan was in effect when the employee sourced the lead? When the opportunity was created? When the quote was issued? When the customer signed? When the order was booked? When the invoice was issued? When the customer paid? When the commission statement was generated? When the employer announced the change? When the employee was terminated? Timing is often the difference between a lawful prospective change and an unlawful retroactive rewrite.

If your employer changed the rules after the sale, read my post: Can My Employer Change My Commission After the Sale in California?

California Labor Code Section 2751 and Written Commission Agreements

Labor Code section 2751 is one of the most important statutes in California commission disputes. It requires written commission agreements for employees rendering services in California when the contemplated method of payment involves commissions. The agreement must explain the method by which commissions are computed and paid. The employer must give a signed copy to the employee and obtain a signed receipt. If the contract expires and the parties continue working under its terms, the terms are presumed to remain in effect until superseded or until employment ends.

This statute is practical. It exists because commission disputes are predictable. Without a writing, employees may rely on oral promises, manager explanations, course of dealing, slide decks, quota emails, sales kickoff presentations, or payroll habits. Employers may later deny or reinterpret those promises. A written plan reduces the room for strategic amnesia. The law does not require commission plans to be simple. It requires the method to be in writing. Of course, a plan can be written and still be a mess. A mess in writing is still a mess; it is just a mess with exhibit numbers.

A Labor Code section 2751 problem can arise when the employer never provided a written plan, failed to obtain a signed receipt, changed the plan without clear notice, relied on oral statements inconsistent with the plan, used formulas that are not actually explained, failed to identify when commissions are earned, failed to identify when commissions are paid, failed to disclose chargeback rules, failed to disclose caps or windfall adjustments, or relied on multiple documents that contradict one another.

Employees sometimes assume that if the employer violated section 2751, every disputed commission is automatically owed. That is too simple. The statute helps the employee, but the remedy analysis depends on the facts and legal claims. A section 2751 violation may support arguments about ambiguity, unlawful wage practices, breach of contract, unfair competition, PAGA penalties, or employer credibility. It may also make it harder for the employer to prove hidden conditions or after-the-fact limits. But employees should still be prepared to prove the commission formula, the sale, the earning conditions, and the amount owed.

The best use of section 2751 in a demand letter is often precise and practical. The employee can ask the employer to identify the written commission agreement, the exact plan language relied upon, the calculation method, the earning condition allegedly not satisfied, the reason for any deduction, the documents showing customer cancellation or nonpayment, and the basis for any cap, windfall adjustment, chargeback, or split-credit decision. Employers who have a lawful explanation should be able to explain it. Employers who cannot explain it often respond with more adjectives. Adjectives are not payroll records.

High-earning employees should treat section 2751 as an evidence tool. Request the written plan. Save all versions. Compare the version you signed against the version the employer now cites. Check dates, signatures, acknowledgments, version numbers, effective dates, change notices, and compensation-plan portals. Employers sometimes rely on a plan document that was uploaded after the dispute began. That does not necessarily prove misconduct, but it is a fact worth knowing.

For more on the practical first steps in a commission dispute, read my post: How Do I Resolve a Commission Dispute in California?

When a Commission Becomes Earned Wages

The most important question in most California commission disputes is when the commission became earned. A commission can be promised, projected, estimated, credited, accrued, advanced, payable, paid, or earned. Those words are not interchangeable. The plan may use them carefully. It may also use them carelessly. Either way, the analysis starts with the plan and then applies California wage law.

A commission is usually earned when the employee satisfies the contractual conditions in the commission plan. Those conditions may include booking the sale, obtaining a signed contract, achieving customer acceptance, generating an invoice, customer payment, expiration of a cancellation period, installation, implementation, revenue recognition, manager approval, or some combination of events. The conditions must be identified before the work is done. The employer generally cannot invent new earning conditions after the employee completes the sale.

California courts have recognized that employers may define when incentive compensation is earned. Cases such as Schachter v. Citigroup, Inc., Lucian v. All States Trucking Co., and Neisendorf v. Levi Strauss & Co. demonstrate that plan conditions can matter, especially when the dispute involves bonuses, stock, or incentive pay subject to continued employment or other conditions. In the commission context, Steinhebel and Koehl show that payments may be structured as advances that are not fully earned until stated conditions occur. But once the conditions are satisfied and the commission becomes wages, the employer’s ability to take it back narrows sharply.

This is where many employers get into trouble. They pay commissions routinely, call them earned in statements, treat the employee as having hit quota, report the sale, count the revenue, and then later claim the payment was only provisional. The plan language must support that position. The employer’s later preference is not a time machine.

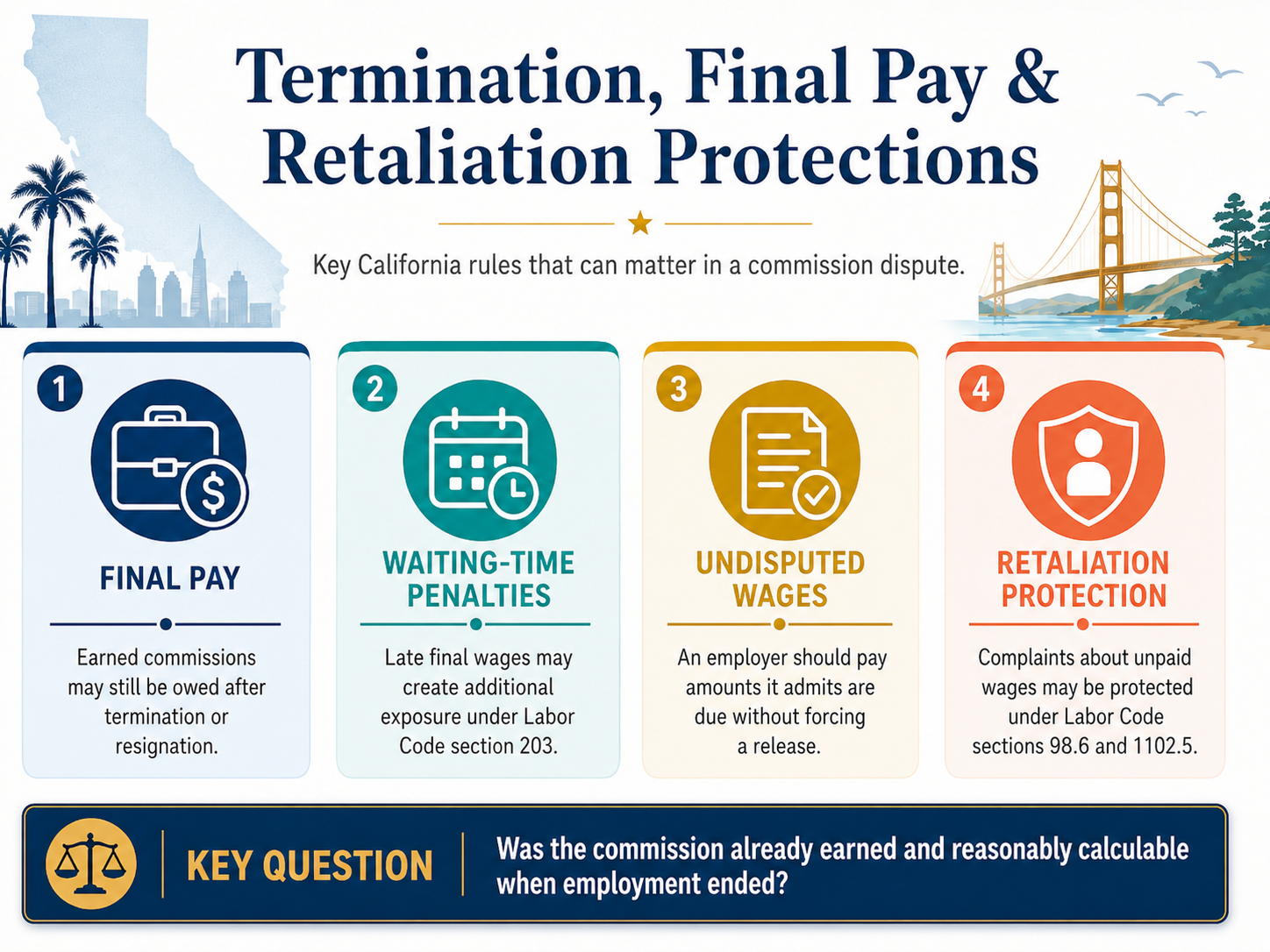

The earned-wage question is especially important after termination. Labor Code section 201 requires immediate payment of earned and unpaid wages when an employee is discharged. Labor Code section 202 requires payment of earned wages to an employee who quits within the statutory time period, generally within 72 hours unless the employee gave at least 72 hours’ notice. Labor Code section 203 imposes waiting-time penalties when an employer willfully fails to pay wages due at separation, up to 30 days of wages. If an earned commission can be reasonably calculated at termination, delayed payment may create significant exposure.

The fact that the employer’s regular commission payout date is later does not always end the analysis. A plan may lawfully pay commissions on a monthly or quarterly cycle, but final-pay statutes can accelerate wages that are already earned and calculable at separation. If the amount is not reasonably calculable at termination because customer payment has not occurred or a cancellation period has not expired, the employer may have a good-faith argument for paying later when the condition occurs. But the employer should not use administrative inconvenience as an excuse to delay wages that are already earned.

Employees should ask: What exactly remained to be done when the employer refused to pay? Was the customer signature obtained? Was the purchase order received? Was the order booked? Was the invoice sent? Did the customer pay? Did implementation actually matter under the plan? Was manager approval a real condition or a rubber-stamp step? Did the employer previously pay commissions before the condition it now says was mandatory? Did the plan say continued employment on the payment date was required? If so, was that condition lawful as applied to an already earned commission?

The employer’s strongest argument is usually that the commission was not yet earned. The employee’s strongest argument is usually that all objective earning conditions were satisfied before the employer withheld, reduced, or took back the money. That is why evidence and timing matter.

If the employer says termination wiped out a deal you already closed, read my post: Closed the Deal, Lost the Commission: California Law on Post-Sale Commission Theft.

Unpaid Commissions After Termination, Resignation, or Layoff

Many commission disputes arise at the end of employment. That is not a coincidence. When the employee is still employed, the employer may try to preserve the relationship. After termination, resignation, layoff, acquisition, or restructuring, the employer has less incentive to keep the employee happy and more incentive to keep the money. The employee also loses access to systems, documents, managers, and internal records. The timing is convenient for the employer. Funny how often convenience wears a badge that says “policy.”

The core rule is straightforward: if the commission was earned, separation does not erase it. California final-pay statutes require prompt payment of earned wages. Labor Code section 201 applies to discharged employees. Labor Code section 202 applies to employees who quit. Labor Code section 203 can impose waiting-time penalties when the employer willfully fails to pay wages due. Labor Code section 206 requires employers to pay undisputed wages without requiring the employee to release disputed claims. Labor Code section 206.5 restricts releases of wage claims when wages are due.

Employers often rely on plan language stating that the employee must be employed on the payout date. Such clauses require careful analysis. A continued-employment condition may be enforceable if the commission was not yet earned and the plan clearly made continued employment part of the earning conditions. But if the employee already earned the commission, a clause that forfeits earned wages because the employee was not employed on a later payout date may be vulnerable. The distinction between earning date and payment date is critical.

For example, assume a plan says the commission is earned when the customer signs a noncancelable contract and the order is booked, but paid the month after customer payment. If the customer signs, the order is booked, the customer pays, and the employee is terminated before the normal pay date, the employer may have a serious problem if it refuses to pay. By contrast, if the plan clearly says the commission is not earned until the customer pays and the customer has not paid by the termination date, the employee may need to wait until the condition occurs, and the dispute may focus on whether the employer later paid correctly.

The case law recognizes that plan conditions matter. In Ellis v. McKinnon Broadcasting Co., the court addressed commissions after termination under a contract that conditioned commissions on customer payment before termination. In other cases involving bonuses or incentive compensation, courts have enforced clear conditions that define when compensation is earned. The employee’s job is to show that the condition the employer relies on does not apply, was satisfied, is ambiguous, was added retroactively, conflicts with other plan language, or improperly forfeits wages already earned.

For a broader discussion of high-value wage claims, read my post: Large Unpaid Wage Claims in California: How to Recover When Your Employer Won’t Pay.

Employees should act quickly after separation. Save plan documents before system access disappears. Export commission statements, quota letters, CRM records, emails, and pay statements. Ask for a written reconciliation. Request the basis for nonpayment. Identify whether the employer admits any amount is owed. Do not sign a severance agreement without analyzing unpaid commissions. Many severance agreements include a broad release of wage, contract, and incentive-compensation claims. Labor Code section 206.5 may limit releases of wages due, but relying on that statute after signing a broad release is not a strategy. It is a litigation hobby.

High-earning employees should be especially careful in severance negotiations. The severance offer may appear generous until the employee realizes it ignores a six-figure or seven-figure commission. Employers sometimes bundle severance, commission disputes, equity issues, nondisparagement, confidentiality, and release terms together. The question is not only whether the severance amount is fair. The question is whether the agreement gives up valuable commission rights.

If commissions are tied up in a severance negotiation, read my post: Severance Negotiation for California Sales Executives: How to Protect Your Bonus, Commission, and Equity.

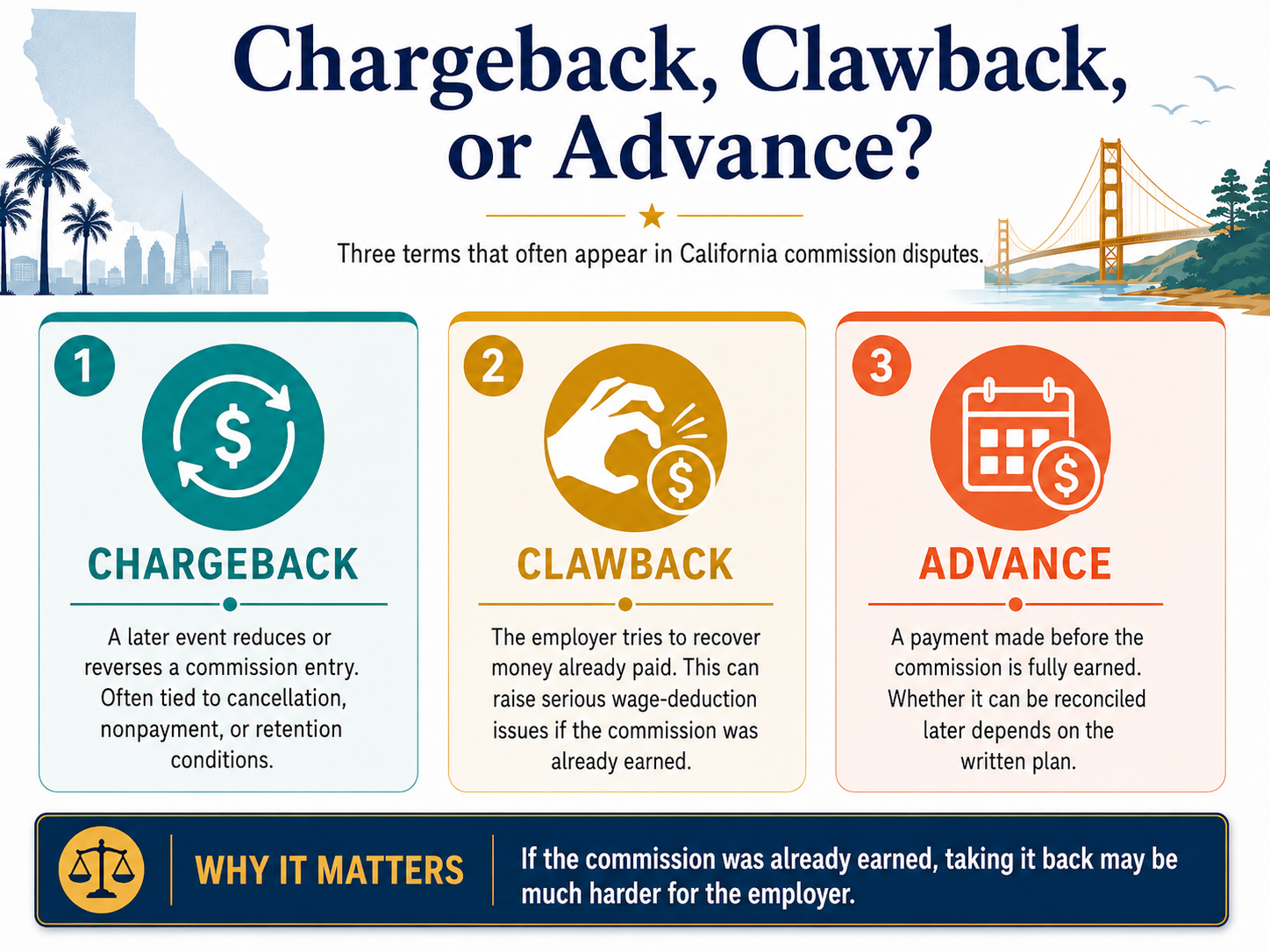

Chargebacks, Clawbacks, Advances, and Deductions

Chargebacks and clawbacks are among the most common commission-dispute issues. They are also among the most abused. The employer pays or credits a commission, then later says the employee must return it or absorb a deduction because the customer canceled, failed to pay, reduced the order, delayed implementation, returned the product, complained, missed a retention period, or triggered a plan rule. Sometimes the employer is right. Sometimes the employer is using the word “chargeback” the way a magician uses smoke.

A lawful chargeback generally depends on the commission not yet being earned or the payment being a clearly disclosed advance subject to lawful recovery. California cases such as Steinhebel v. Los Angeles Times Communications, LLC and Koehl v. Verio, Inc. recognized that employers can structure commission payments as advances against future earned commissions when the plan clearly explains the conditions. If the customer must remain subscribed for a stated period, pay the invoice, or satisfy a retention requirement before the commission is earned, the employer may be able to reconcile an advance if the condition fails.

But the rules change once a commission is earned wages. Labor Code section 221 prohibits employers from collecting or receiving from an employee any part of wages previously paid. Labor Code section 223 prohibits secret underpayment where a wage scale is promised. Labor Code section 224 allows certain authorized or legally required deductions, but it does not give employers a free pass to take back earned wages through a broad authorization. Labor Code section 225.5 provides civil penalties for certain unlawful wage withholding violations, including violations of sections 221 and 223.

Sciborski v. Pacific Bell Directory illustrates the danger of improper deductions. The employee alleged that the employer deducted wages to recover a commission after the employer decided the commission should not have been paid. The case is often cited in commission-chargeback discussions because it shows that employers cannot simply reach into wages to recover amounts they later regret paying.

For a focused explanation of chargebacks, read my post: What Is a Commission Chargeback in California?

The employee should ask several questions:

- Did the plan clearly identify the payment as an advance before it was paid?

- Did the plan clearly explain the condition that later failed?

- Was the condition objective and measurable?

- Was the chargeback tied to the specific transaction or used to offset ordinary business costs?

- Did the employer deduct from future commissions, base wages, final wages, PTO, or other compensation?

- Did the employee sign a lawful written authorization, and did the deduction amount to a rebate or deduction from wages?

- Did the employer apply the rule consistently?

- Did the employer cause the cancellation, nonpayment, implementation delay, or return?

- Was the chargeback imposed after the commission was already earned?

- Did the employer provide a reconciliation?

Chargebacks used to shift ordinary business losses to employees are especially suspect. Employers may attempt to deduct for product returns, customer bankruptcy, implementation failures, discounts approved by management, sales tax errors, shipping costs, financing delays, customer support problems, credit-card fees, customer incentives, or pricing concessions. Some conditions may be valid if written clearly and tied to earning the commission. But an employer generally cannot use commission chargebacks as a general business-loss insurance policy funded by employees.

For more on proving an unlawful chargeback, read my post: Proving Commission Chargebacks Are Illegal in California: A Guide for Employees.

A common red flag appears when the plan says the commission is earned upon sale but also says it can be charged back for nearly any later reason. A commission cannot be fully earned and endlessly unearned at the same time unless the plan clearly defines a provisional advance structure. If the employer wants money to remain conditional, it must say so clearly before the employee performs the work.

Another red flag appears when the employer deducts a chargeback from final pay after termination. Final wages are subject to strict rules. An employer should not treat the last paycheck as a convenient closing drawer. If the employer believes the employee owes money, it may need to pursue that claim separately rather than self-help through wage deductions.

For a step-by-step approach to fighting chargebacks, read my post: How to Fight Illegal Commission Chargebacks Like an Employment Lawyer.

Windfall Provisions, Commission Caps, and Employer Discretion

A windfall provision is plan language that allows an employer to reduce, cap, review, or adjust commissions when the calculated payout is unusually large, exceeds a threshold, results from a special transaction, arises from an account reassignment, exceeds a percentage of quota, or would be disproportionate to the employee’s expected compensation. The employer’s position is usually that the employee should not receive an unexpectedly large commission from a deal the company views as abnormal. The employee’s position is usually that the plan promised a formula, the employee delivered the sale, and the employer only discovered “fairness” after seeing the size of the check.

Both sides may have arguments. California law does not automatically ban every windfall provision or commission cap. A plan can include caps, caps by product line, accelerators that stop at a threshold, special deal review, house-account exclusions, large-deal provisions, or windfall adjustments if the rules are clearly written and disclosed in advance. The legal problem arises when the employer invokes discretion after the employee has satisfied the earning conditions, relies on vague language to rewrite the formula, applies the rule inconsistently, hides the cap, or uses a windfall label to avoid paying earned wages.

The recent published decision in Sorokunov v. NetApp, Inc. is important for this topic. In that case, the employee challenged a windfall clause in a commission plan after NetApp reduced additional commissions on a deal that exceeded a threshold. The Court of Appeal affirmed the arbitration outcome for the employer, concluding that the written plan disclosed the windfall adjustment mechanism, the employer had not taken back wages already paid, and Labor Code section 2751 required the commission method to be in writing but did not prohibit every discretionary component. The case is significant because it warns employees not to assume that all windfall provisions are unlawful.

But Sorokunov should not be read as a blank check for employers. A windfall clause still needs careful review. Was it clearly written? Was it provided before the sale? Did the plan define when commissions were earned? Did the employer apply the clause before the commission became wages? Did the employer disclose the adjustment method? Did the employee receive a signed copy? Did management follow the procedure? Did the clause conflict with other plan language? Did the employer use the clause only after the amount became inconvenient? Did the plan say the adjustment could be made for “any reason” without standards? Did the employer use the windfall clause to take back wages already paid?

For a deep dive on windfall provisions, read my post: California Commission Clawback Lawyer for Employees: Windfall Provisions, Commission Caps, and Unpaid Sales Commissions.

Commission caps raise similar issues. A cap may limit commissions after the employee reaches a dollar amount, percentage of quota, or total payout threshold. A clearly written prospective cap is more likely to be enforced than a cap announced after the deal closes. The strongest employee cases often involve caps that were not in the plan, caps added midstream, caps hidden in a policy never provided to the employee, caps applied differently to different employees, or caps imposed after the employer previously confirmed the uncapped commission.

Employer discretion also requires scrutiny. A plan may say commissions are subject to management approval, finance review, compensation committee review, or executive discretion. But discretion is not the same as whim. California law recognizes the implied covenant of good faith and fair dealing in contracts. If an employer has discretion under a commission plan, the employee may argue the employer cannot exercise that discretion arbitrarily, in bad faith, contrary to the plan’s purpose, or solely to deprive the employee of compensation earned through performance.

Practical example:

A plan pays 8 percent of annual contract value on new enterprise sales, with accelerators above quota. The employee closes a $12 million contract after nine months of work. The employer then says the deal was a “windfall” because procurement expanded the order to include additional business units. The plan contains no windfall clause, no cap, and no discretion clause. That is a strong employee fact pattern. By contrast, if the plan says any transaction exceeding 200 percent of annual quota is subject to written windfall review before commissions are earned, and the employer applies the same formula it has used consistently, the employer’s argument improves.

Matt’s Legal Perspective: Windfall provisions are where commission law meets corporate embarrassment. The employer wrote the plan. The employee followed it. The deal got bigger than expected. Now everyone is suddenly a philosopher. The legal question is not whether the commission feels large. The legal question is what the plan said before the work was done and whether wage law permits the adjustment.

Post-Sale Changes, Quota Manipulation, Accelerators, and Moving Targets

Some of the strongest commission disputes involve post-sale changes. The employee closes the deal, then the employer changes the quota, lowers the rate, removes an accelerator, reclassifies the account, changes territory credit, reassigns the customer, excludes part of the transaction, announces a cap, or says the plan was never intended to apply to that kind of sale. The timing is the issue. Prospective plan changes may be lawful. Retroactive changes to earned commissions are much more dangerous.

California law generally allows employers to change compensation terms prospectively, provided the change is lawful, disclosed, and not retaliatory or discriminatory. But an employer cannot wait until after the employee earns a commission and then rewrite the conditions to reduce wages. Once earned, the commission is protected as wages. Labor Code section 221 restricts wage takebacks, and final-pay statutes require prompt payment of earned wages at separation.

Quota manipulation is common in high-value sales. Employers may set a quota, watch the employee approach accelerators, and then raise the quota or change attainment rules. A plan may allow quota adjustments for territory changes, acquisitions, product launches, or data errors. But the employer should not use quota changes as a moving target designed to avoid accelerators after performance occurs. Employees should document the original quota, the date of any change, who approved the change, whether the plan allowed it, whether the change was prospective, and whether similarly situated employees were treated differently.

Accelerators are another frequent battleground. An accelerator rewards overperformance by increasing the commission rate after the employee exceeds quota. Employers love accelerators when they motivate employees. They love them less when employees actually accelerate. A dispute may arise when the employer claims the employee did not cross the threshold, the deal should be excluded, quota should be reset, the customer should be split, a cap applies, or the accelerator was discretionary. Again, the written plan and timing are central.

Post-sale reclassification also happens. The employer may say a deal is a renewal rather than new business, services rather than software, channel rather than direct, house account rather than assigned account, strategic account rather than territory account, noncommissionable product rather than eligible product, or company-sourced rather than employee-sourced. Some classifications may be legitimate. But if the reclassification appears only after a large commission is due, the employee should investigate.

Common red flags include: the employer cannot identify the plan provision supporting the change; the change occurred after the customer signed; the employer previously paid similar deals differently; the commission statement originally showed a higher amount; a manager confirmed the payout in writing; finance changed the calculation without explanation; the employer refuses to provide backup; the plan reserves discretion but gives no standard; the employee was terminated shortly before payment; or the employer offers severance in exchange for a broad release.

Practical tip:

Create a before-and-after chart. Column one should list the original plan term. Column two should list the employer’s new position. Column three should identify the date the employer announced the new position. Column four should list the evidence contradicting it. This turns a vague fairness argument into a timeline. Timelines are useful because they make hindsight look like hindsight.

For a focused discussion of post-sale commission changes, read my post: Can My Employer Change My Commission After the Sale in California?

High-Earning Employee Commission Disputes

High-earning employees face unique commission-dispute problems. The larger the payout, the more motivated the employer may be to reduce it. This is especially true in enterprise software, medical device sales, biotechnology, life sciences, financial services, telecommunications, cloud infrastructure, cybersecurity, advertising technology, commercial real estate-adjacent employment roles, and executive sales management. In those fields, one transaction can produce a commission that exceeds the employee’s base salary, annual target compensation, or even several years of ordinary earnings.

Large commission disputes often involve more than payroll. They involve executive leadership, finance, legal, HR, sales operations, revenue recognition, customer success, implementation, and sometimes the board. The employer may claim the commission is disproportionate to effort, the deal was company-sourced, the customer was inherited, the discount was too large, the transaction was nonstandard, the product mix changed, the account was strategic, the contract term was unusual, the customer has not fully paid, or the employee was not responsible for the final expansion.

Employees should be prepared for employer defenses that sound business-oriented rather than legal. The employer may say paying the commission would violate internal equity, damage compensation budgets, create bad precedent, overpay the employee relative to peers, reduce EBITDA, affect acquisition metrics, distort the sales compensation model, or create a windfall. Those explanations may matter if the plan gives the employer discretion. But if the plan promised a formula and the employee satisfied it, the employer’s budget discomfort does not rewrite California wage law.

For a real-world example of a seven-figure commission dispute, read my post: Recovering Unpaid Commissions in California: $1M Case Study.

High earners should not underestimate the importance of professional tone. A large commission dispute can become emotional quickly, particularly when the employee believes leadership is acting in bad faith. But angry emails rarely improve leverage. The better approach is disciplined and document-driven: identify the plan, quote the earning language, summarize the sale, attach supporting documents, request a calculation, ask for the specific basis for nonpayment, and reserve rights. The goal is to look like the reasonable party. In litigation, reasonable is underrated and screenshots are forever.

High earners should also examine related compensation rights. A termination or resignation may affect unpaid commissions, bonuses, overrides, equity, RSUs, stock options, deferred compensation, retention payments, severance, expense reimbursements, PTO, and indemnity rights. The employer may try to resolve all issues in one separation agreement. Do not analyze the commission dispute in isolation if the release would cover other valuable claims.

Another issue for high earners is arbitration. Many executives and sales employees signed arbitration agreements. Arbitration can change procedure, discovery, cost allocation, confidentiality, class or representative claims, and settlement leverage. Arbitration does not eliminate California wage law, but it can change how the dispute is fought. Employees should review the arbitration agreement early, especially if the claim is large enough to justify litigation.

Matt’s Practical Tip:

If the commission number is big enough that finance suddenly becomes poetic, get legal advice before you send the long email. The first written dispute often becomes Exhibit A. Make Exhibit A boring, accurate, and devastating.

Sales Credit Disputes, Split Commissions, Territory Changes, and House Accounts

Commission disputes are not always about whether a sale occurred. Sometimes everyone agrees the customer bought the product. The fight is over who gets credit.

Sales credit disputes are common in large organizations with account executives, sales development representatives, sales engineers, overlays, channel managers, regional managers, customer success teams, account managers, renewal representatives, product specialists, and executives. Multiple people may contribute to a deal. The plan should explain how credit is assigned and split. If it does not, the dispute may turn on written communications, CRM ownership, territory records, manager approvals, course of performance, and company practice.

Split-commission disputes often arise when one employee sources the lead, another manages the relationship, a third handles the technical sale, and a manager reallocates credit near closing. The employer may claim the plan gives it discretion to allocate credit. The employee may argue that the allocation was inconsistent, retaliatory, discriminatory, contrary to the plan, or made after the commission became earned.

Territory changes are another major issue. A company may remove a lucrative account from the employee’s territory, reassign a region, move strategic accounts to a national team, create house accounts, or shift customers to a new sales unit. Prospective territory changes may be lawful. But if the employee already performed the work and satisfied the earning conditions, a later territory change should not erase earned wages. The critical question is whether the territory change occurred before or after the employee earned sales credit under the plan.

House accounts deserve special attention. Employers often designate certain customers as house accounts, meaning no ordinary commission is paid or only a reduced commission applies. A house-account rule is easier to defend when disclosed before the employee works the account. It is harder to defend when the employer labels the account “house” only after the employee develops the opportunity.

Channel and partner deals raise similar problems. The employer may say the transaction was partner-sourced and therefore paid at a lower rate. The employee may argue that the partner merely processed paperwork after the employee generated the opportunity. The evidence may include CRM entries, partner registration records, email chains, meeting notes, demo records, quote history, customer communications, and manager approvals.

Overlay roles can be especially messy. An overlay salesperson may earn credit for selling a product line into accounts owned by other account executives. If the plan does not clearly define overlay credit, the employer may later argue that the overlay only gets paid when the primary account executive receives credit, or only when the product is coded correctly. Again, written rules and actual practice matter.

Employees should document sales credit early. Do not wait until payout. Save CRM screenshots showing opportunity owner, split percentages, territory assignment, product codes, amount, close date, stage history, and approval history. Save emails confirming credit. Ask managers to confirm split-credit decisions in writing. The best time to prove credit is before the deal becomes valuable enough for others to discover their deep historical connection to it.

Evidence: How to Audit and Prove Your Commission Claim

A commission dispute is won or lost on documents. Memory matters, but documents usually decide leverage. Employees should build a commission audit file as soon as a dispute appears. The goal is to reconstruct the plan, the sale, the calculation, the employer’s explanation, the timeline, and the damages.

Start with compensation documents. Save the offer letter, employment agreement, commission plan, quota letter, annual incentive plan, sales compensation terms, amendments, plan acknowledgments, plan portal screenshots, emails announcing plan changes, sales kickoff decks, FAQ documents, manager explanations, and any policy describing sales credit, chargebacks, windfalls, caps, or accelerators.

Next, gather sales documents. Save the signed customer agreement, purchase order, statement of work, renewal order, amendment, quote, pricing approval, discount approval, order form, booking confirmation, invoice, payment confirmation, customer acceptance, implementation milestone, and renewal confirmation. If you cannot access customer documents, save CRM screenshots and emails showing the same information.

Then gather calculation documents. Save commission statements, pay statements, payroll records, W-2s, spreadsheets, commission portal screenshots, quota-attainment reports, dashboards, accelerator calculations, finance reconciliations, sales operations reports, and any email explaining the payment. If the employer later changes the numbers, preserve the earlier version. Version history can be gold. It can also be terrifying, depending on who edited cell H47.

Create a timeline. Identify the dates of plan issuance, plan acknowledgment, quota assignment, lead creation, opportunity creation, customer meetings, quote issuance, contract signature, booking, invoicing, customer payment, commission statement, payment date, employer adjustment, employee complaint, HR response, termination, and final paycheck. Commission disputes often turn on whether the employer acted before or after the commission was earned.

Ask for a reconciliation. A professional written request might say: “I am requesting a written reconciliation of the commission calculation for the ABC account. Please identify the plan provision relied upon, the gross or net revenue used, the applicable rate, any quota or accelerator calculation, any deductions or exclusions, any windfall or cap provision applied, and any documents supporting the adjustment.” This is not hostile. It is what a serious employee asks when the paycheck is wrong.

Preserve communications. Do not delete emails, texts, Slack messages, Teams messages, voicemails, calendar invites, or notes. Do not take confidential documents unlawfully, do not access systems after authorization ends, and do not forward trade secrets to personal accounts without legal advice. Employees need evidence, but evidence collection should be lawful and careful. The goal is to build a case, not create a new problem wearing a trench coat.

If you are still employed, consider whether to consult an attorney before escalating. The way you raise the issue can affect retaliation protection, settlement leverage, and future litigation. A well-written wage complaint can be protected activity. A long emotional accusation may still be protected in some circumstances, but it may also distract from the merits. Keep the focus on wages owed, plan terms, and documents.

For more on making a professional wage demand, read my post: How to Demand Unpaid Wages Like an Employment Lawyer.

How to Raise a Commission Dispute While Protecting Yourself From Retaliation

Employees often hesitate before raising commission disputes because they fear retaliation. That fear is rational. Commission disputes usually involve money, and money has a way of making employers suddenly sensitive. California law provides protections, but legal protection does not prevent every employer from reacting badly. It gives the employee remedies if retaliation occurs and can improve leverage when the employee documents the issue correctly.

Labor Code section 98.6 prohibits employers from discharging, discriminating, retaliating, or taking adverse action against employees because they made written or oral complaints that they are owed unpaid wages, filed claims, initiated proceedings, or exercised protected rights. The statute also provides a rebuttable presumption in favor of the employee’s retaliation claim when the employer takes prohibited action within 90 days of protected activity. Labor Code section 1102.5 protects employees who disclose information to someone with authority to investigate, discover, or correct a violation when the employee reasonably believes the information discloses a legal violation.

The best first complaint is usually factual, written, and narrow. Identify the commission, the amount you believe is owed, the plan language, the sale, and the documents. Ask for a written explanation. Avoid insults. Avoid speculation about motives. Avoid threats. Avoid copying half the company unless there is a strategic reason. The first email should read like something a judge, arbitrator, HR investigator, or opposing counsel can understand in five minutes.

A strong internal complaint might include:

- The commission period and customer or deal name

- The commission plan and version date

- The specific plan language supporting payment

- The formula and your calculation

- The amount paid and amount missing

- The employer explanation, if any

- A request for reconciliation and supporting documents

- A statement that you are raising a good-faith wage issue

- A request that the company preserve relevant records

Employees should also document any retaliation. Retaliation can include termination, demotion, suspension, reduced territory, removal from accounts, quota manipulation, exclusion from meetings, negative write-ups, threats, reduced leads, reduced support, withholding expense reimbursement, sudden performance criticism, or pressure to sign a release. Not every negative event is retaliation, but timing and context matter.

If the employer responds professionally and fixes the issue, excellent. That is the rare happy ending, like finding a clean conference room at 4 p.m. If the employer refuses, delays, threatens, or changes your role, consult counsel promptly. The dispute may now involve both unpaid wages and retaliation.

If you are worried about retaliation after raising unpaid wages, read my post: How Do I Ask for Unpaid Wages Without Getting Fired?

Legal Claims, Remedies, Penalties, and Attorney Fees

A commission dispute may involve several legal theories. The right theory depends on the facts, plan language, timing, and amount at stake. Common claims include unpaid wages, breach of contract, unlawful deductions, waiting-time penalties, statutory penalties, unfair competition, retaliation, wrongful termination in violation of public policy, declaratory relief, accounting, and claims under an arbitration agreement or representative statute where applicable.

Unpaid wages are the core claim when the commission was earned but not paid. Labor Code section 200 defines wages broadly. Labor Code section 204 governs regular wage timing. Labor Code sections 201 and 202 govern final pay. Labor Code section 203 provides waiting-time penalties for willful failure to pay wages due at separation, up to 30 days of wages. Labor Code section 206 requires payment of undisputed wages without conditioning payment on a release. Labor Code section 206.5 restricts releases of wage claims where wages are due.

Unlawful deduction claims may arise under Labor Code sections 221, 223, 224, and 225.5. Section 221 prohibits employers from collecting back wages previously paid. Section 223 prohibits secretly paying less than the wage scale while purporting to pay the designated wage. Section 224 permits certain deductions required by law or expressly authorized in writing, but not deductions that amount to an improper rebate or wage deduction. Section 225.5 authorizes civil penalties for certain unlawful withholding violations.

Breach of contract claims may apply when the employer violated the written commission plan. Contract interpretation principles under the Civil Code may become important when plan language is ambiguous, contradictory, or incomplete. The implied covenant of good faith and fair dealing may also matter when the employer has discretion and allegedly uses it to deprive the employee of compensation.

Unfair competition claims under Business and Professions Code section 17200 may apply when unlawful wage practices constitute unlawful or unfair business practices. Business and Professions Code section 17203 allows restitution and injunctive relief in appropriate cases, and section 17208 provides a four-year limitations period for UCL claims. UCL remedies are equitable and not identical to wage damages, but they can be useful in some commission disputes.

Retaliation claims may arise under Labor Code section 98.6, Labor Code section 1102.5, or other statutes depending on the facts. If the employee was fired or punished for complaining about unpaid commissions, the retaliation claim may become as important as the wage claim. Remedies may include lost wages, work benefits, reinstatement in some cases, civil penalties, attorney fees under certain statutes, and other relief.

Attorney-fee provisions matter. Labor Code section 218.5 permits attorney fees and costs to the prevailing party in certain actions for nonpayment of wages, but an employer can recover fees only if the employee brought the action in bad faith. Labor Code section 1102.5 authorizes reasonable attorney fees to a successful plaintiff. Contractual fee provisions, arbitration agreements, and statutory claims can also affect fee recovery.

Employees should also consider the forum. Options may include an internal demand, attorney demand letter, Labor Commissioner claim, civil lawsuit, arbitration, mediation, or settlement negotiation. The Labor Commissioner may be practical for smaller and simpler wage claims. Large commission disputes, executive compensation disputes, complicated chargeback cases, and claims involving retaliation or arbitration often require a more strategic approach.

Statutes of limitation require attention. Different claims have different deadlines, and deadlines can depend on whether the claim is statutory, contractual, equitable, or tied to penalties. Employees should not wait. Delay can also cause evidence problems, witness memory problems, and leverage problems. In commission cases, time does not heal all wounds. Sometimes it just deletes Slack history.

For more on litigation options while still employed, read my post: Can I Sue My Employer for Unpaid Wages in California While Still Employed?

Case Studies and Practical Examples

The following case studies are written as educational examples. Some are hypothetical composites based on common commission-dispute patterns. One references the Ruggles Law Firm’s published $1 million unpaid commission case study. These examples are not legal advice and do not predict outcomes. Commission disputes depend on the exact plan language, facts, documents, and timing.

Case Study 1: The Enterprise Software Windfall Clause

An account executive closes a $15 million SaaS contract after a year-long sales cycle. The written plan pays 8 percent of annual contract value and includes accelerators above quota. After close, finance says the payout is “too large” and invokes a windfall clause buried in a global sales policy. The employee signed the annual plan but never received the global policy. The commission statement initially showed the full payout, then changed after executive review.

The legal analysis would focus on whether the windfall provision was part of the written commission contract, whether Labor Code section 2751 was satisfied, when the commission was earned, whether the employer applied the clause before or after wages were earned, whether the clause was clear, and whether the employer used discretion in good faith. The employee’s evidence should include the signed plan, portal history, sales credit approvals, commission statements, emails about the deal, and proof that the policy was not provided.

Case Study 2: The Medical Device Territory Reassignment

A medical device sales representative develops a hospital system for two years. Shortly before a major purchase order, the employer reassigns the hospital to a national accounts team and says the employee is not entitled to commission because the account is now strategic. The plan allows territory changes but does not address already-developed opportunities.

The dispute would turn on timing and sales credit. If the territory changed before the employee earned commission credit, the employer may have an argument. If the employee already satisfied plan conditions for credit, a later reassignment may not erase earned wages. The employee should preserve account-development records, emails with hospital contacts, CRM history, territory maps, forecast submissions, manager approvals, and the timing of the reassignment.

Case Study 3: The Customer Payment Condition

A sales employee closes a transaction, but the customer does not pay for 90 days. The plan says commissions are earned only upon customer payment. The employee resigns before payment. When the customer later pays, the employer says no commission is owed because the employee was not employed on the pay date.

This case turns on whether continued employment was an earning condition or only a payment-date condition, and whether the commission became earned when the customer paid. If the plan clearly required employment at the time of customer payment as part of earning, the employer’s argument may improve. If the plan merely paid commissions later for administrative convenience, the employee’s argument improves. The distinction between earning and payment date is critical.

Case Study 4: The Chargeback for Employer-Caused Implementation Failure

A technology salesperson earns a commission after booking a customer. The plan allows chargebacks if the customer cancels before implementation. The customer cancels because the employer’s implementation team missed deadlines and could not deliver promised features. The employer charges back the commission.

The legal question is whether the chargeback condition applies when the cancellation was caused by the employer rather than the employee or customer. The employee may argue the employer cannot use its own failure to deprive the employee of compensation, especially if the plan does not clearly assign that risk to the employee. Evidence should include customer complaints, implementation tickets, internal emails, and manager admissions about product delays.

Case Study 5: The Split Commission Reallocation

Two employees work on a deal. The CRM shows a 70/30 split for months. After the deal closes, a senior manager reallocates the split to 30/70 because one employee is leaving the company. The plan gives management discretion over splits but says splits should be documented before close.

The employee should focus on the documented split, timing of the change, reason for the change, plan discretion, past practice, and whether the reallocation was retaliatory or designed to avoid paying a departing employee. A discretion clause does not necessarily permit arbitrary or bad-faith changes.

Case Study 6: The Accelerator That Vanished

A salesperson exceeds annual quota by 180 percent. The plan provides an accelerator after 100 percent of quota. After year-end, the employer raises the quota retroactively based on “market opportunity,” eliminating the accelerator. The plan allows quota changes for territory adjustments but the employee’s territory did not change.

This is a classic moving-target dispute. The employee should gather the original quota, quota-approval emails, attainment reports, plan language, timing of the change, and evidence that the territory did not change. A prospective quota adjustment may be lawful. A retroactive adjustment designed to erase an earned accelerator is much more problematic.

Case Study 7: The House Account Surprise

A sales employee is assigned a major customer, manages the relationship, and closes an expansion. After close, the employer says the customer was actually a house account and not commissionable. The plan excludes house accounts but does not list them. The customer appeared in the employee’s territory reports for two years.

The employee should ask for the house-account list, the date the customer was designated house, who approved the designation, and why the customer was assigned to the employee if no commission could be earned. Evidence of territory reports, quotas including the account, forecasts, and manager instructions may support the employee’s claim.

Case Study 8: The Severance Release Trap

A regional vice president is laid off and offered severance. The agreement includes a broad release of all wage, bonus, commission, equity, and contract claims. The employer says commissions will be handled “in the ordinary course,” but refuses to list the amounts. The employee has a pending six-figure override from a team deal.

The employee should not sign until the commission issue is resolved or expressly preserved. The severance agreement should address unpaid commissions, overrides, payment dates, calculation method, disputed amounts, and any release carve-outs. Severance negotiations for sales executives often turn on the compensation the employer left out, not just the severance number it offered.

Case Study 9: The Renewal Versus New Business Fight

An account executive closes a large expansion with an existing customer. The employee treats it as new business because the expansion adds new products and new users. The employer pays it as a renewal at a lower rate. The plan defines renewal, expansion, upsell, and new logo poorly.

This dispute is about classification. The employee should compare plan definitions, product codes, quote history, prior commission treatment, sales operations guidance, and manager emails. Ambiguous definitions may be interpreted against the drafter, particularly if the employer applied the terms inconsistently.

Case Study 10: The Manager Approval Delay

A plan says commissions require manager approval. The employee closes the deal and the manager approves it in the CRM, but finance delays final approval for months. The employee is then terminated and the employer says final approval never occurred.

Approval conditions should be analyzed carefully. If approval was a ministerial step and the employee satisfied all substantive conditions, the employer may not be able to use delay as a forfeiture device. The employee should preserve CRM approvals, emails, workflow screenshots, and evidence that similar deals were paid without additional approval.

Case Study 11: The Customer Discount Deduction

The employer approves a discount to win a strategic account. After the deal closes, finance reduces the salesperson’s commission because the discount lowered margin. The plan pays on gross bookings and does not mention discount-based reductions.

If the plan pays on gross bookings, the employer may have difficulty imposing a margin adjustment after the sale. If the plan pays on gross margin or net revenue, the employer’s argument may improve. The employee should identify the precise commission base and whether discounts were already baked into the rate.

Case Study 12: The Draw Against Commission Problem

An employee receives a monthly draw. The plan says the draw is recoverable from future commissions but does not say the employee must repay a deficit after termination. The employee leaves with a negative balance and the employer deducts it from final wages.

Draw plans must be reviewed closely. A recoverable draw may be offset against future commissions if the plan says so. But deducting from final wages or demanding repayment after termination may raise different issues. The employee should examine the written authorization, plan language, Labor Code section 224, and whether the draw was treated as wages or an advance.

Case Study 13: The Acquisition Cleanup Plan

A company preparing for acquisition changes commission rules to improve financial statements. It reclassifies prior commissions as advances, imposes new retention conditions, and slows payment of large deals. Employees are told the change is necessary for “deal hygiene,” which sounds clean but often is not.

The key question is whether the employer is changing future compensation or retroactively impairing earned commissions. Acquisition-related pressure does not suspend wage law. Employees should preserve old plans, new plans, announcement emails, acquisition communications, and payment history.

Case Study 14: The Executive Override Dispute

A VP of Sales has an override on regional revenue. The company removes several large accounts from the region after the deals are substantially complete and says the VP does not receive override credit. The plan gives the company authority to define regions but also says overrides are earned when revenue is booked in the assigned region.

The dispute would focus on region definition, timing, booked revenue, whether account removal was prospective, whether the VP had already earned the override, and whether the employer acted in good faith. Executive-level plans often have more discretion, but they are still contracts and may involve wage rights.

Step-by-Step Action Plan for Employees

If you are facing a commission dispute, do not begin by arguing about fairness. Fairness matters, but the first round should be documents, math, and timing.

Step 1:

Get every compensation document. Pull the commission plan, quota letter, offer letter, employment agreement, plan amendments, policy documents, sales crediting rules, chargeback provisions, windfall provisions, and any severance or release document.

Step 2:

Identify the earning condition. Underline the plan language that says when the commission is earned. Separate earning conditions from payment timing. If the plan is unclear, note the ambiguity.

Step 3:

Reconstruct the sale. Gather CRM records, quotes, signed contracts, purchase orders, invoices, customer payment information, implementation records, account notes, approval emails, and commission statements.

Step 4:

Calculate your amount. Use the employer’s own formula where possible. Show the rate, commission base, quota, accelerator, split, cap, deduction, and amount owed. If you cannot calculate exactly because the employer controls data, explain what data is missing.

Step 5:

Request a written reconciliation. Ask the employer to identify the plan language, formula, data, deductions, and reason for nonpayment. Keep the request professional and factual.

Step 6:

Preserve evidence and access. Save documents lawfully before access ends. Do not access systems without authorization. Do not take trade secrets. Do not delete communications.

Step 7:

Watch for retaliation. Document any adverse action after you complain. If you are still employed, be deliberate about tone and timing.

Step 8:

Do not sign a release casually. Severance agreements can release commission claims. Analyze unpaid commissions before signing.

Step 9:

Consult counsel if the amount is significant. A large commission dispute can involve wage law, contract law, retaliation law, arbitration, attorney fees, and settlement strategy. Early legal review can prevent costly mistakes.

Step 10:

Act before leverage fades. Deadlines matter, evidence disappears, and memories get polished. Delay usually helps the party holding the money.

If your employer withheld, reduced, capped, or clawed back commissions you believe you earned, contact Ruggles Law Firm at 916-758-8058 for a confidential evaluation.

Bring the commission plan, the commission statement, the disputed calculation, and any written explanation from the employer. The more documents you bring, the less everyone has to guess.

Guessing is for carnival games, not wage claims.

Frequently Asked Questions: California Commission Disputes

These answers provide general California information. Individual facts, commission plans, employers, statutes, and deadlines can change the analysis.

What is a commission dispute in California?

A commission dispute is a disagreement over whether an employee earned commissions, how commissions should be calculated, when they must be paid, or whether the employer can reduce, cap, claw back, or withhold them. In California, the dispute usually turns on the written commission plan, Labor Code wage protections, and the facts showing whether the employee satisfied the earning conditions.

Are commissions considered wages in California?

Yes, once earned, commissions are generally treated as wages under California law. Labor Code section 200 broadly defines wages to include compensation for labor performed, including compensation measured by commission. The key question is when the commission became earned under the written plan.

What law requires written commission agreements in California?

Labor Code section 2751 requires a written commission contract for employees who render services in California when the contemplated payment method involves commissions. The contract must set forth the method by which commissions are computed and paid, and the employer must provide a signed copy and obtain a signed receipt.

What should a written commission agreement include?

A proper commission agreement should identify the commission formula, eligible sales, rate, quota, accelerator, cap, earning conditions, payment timing, chargeback rules, sales credit rules, treatment after termination, and dispute process. If the plan omits key terms, the ambiguity may become important in a dispute.

What happens if my employer never gave me a written commission plan?

The lack of a written plan can help your claim, but it does not automatically prove every commission is owed. You may still need to prove the promise, the sales, the formula, the amount owed, and the employer’s failure to pay. Emails, offer letters, commission statements, pay history, and manager admissions can become important evidence.

When is a commission earned in California?

A commission is usually earned when the employee satisfies the conditions stated in the commission plan. Those conditions may include booking, customer signature, invoicing, payment, retention, implementation, or another objective event. The employer generally cannot invent new earning conditions after the employee performs the work.

Can my employer delay commission payment after I earned it?